One in four new cars sold globally is now electric. But the story behind that headline is a tale of strikingly different speeds — and Australia is finally finding its stride. Here’s where every major market stands, what it means, and what comes next.

A world in transition — at wildly different speeds

The electric vehicle revolution is real, it’s accelerating, and it is reshaping the global car market in ways that would have seemed fantastical just five years ago. According to the International Energy Agency’s Global EV Outlook 2026, electric car sales grew by 20% globally last year to exceed 20 million units — meaning one in every four new cars sold worldwide now runs on a battery. For context, that is roughly five times the share EVs held just four years ago.

But dig beneath that 25% global headline, and three very different worlds emerge: a China that is barrelling toward an electric majority, a Europe accelerating hard on the back of tightened regulation, and a United States pulling in the opposite direction as federal incentives evaporate. And then there is Australia — a market that spent years lagging embarrassingly behind, only to find itself charging up the ranks in 2026 at a pace few predicted.

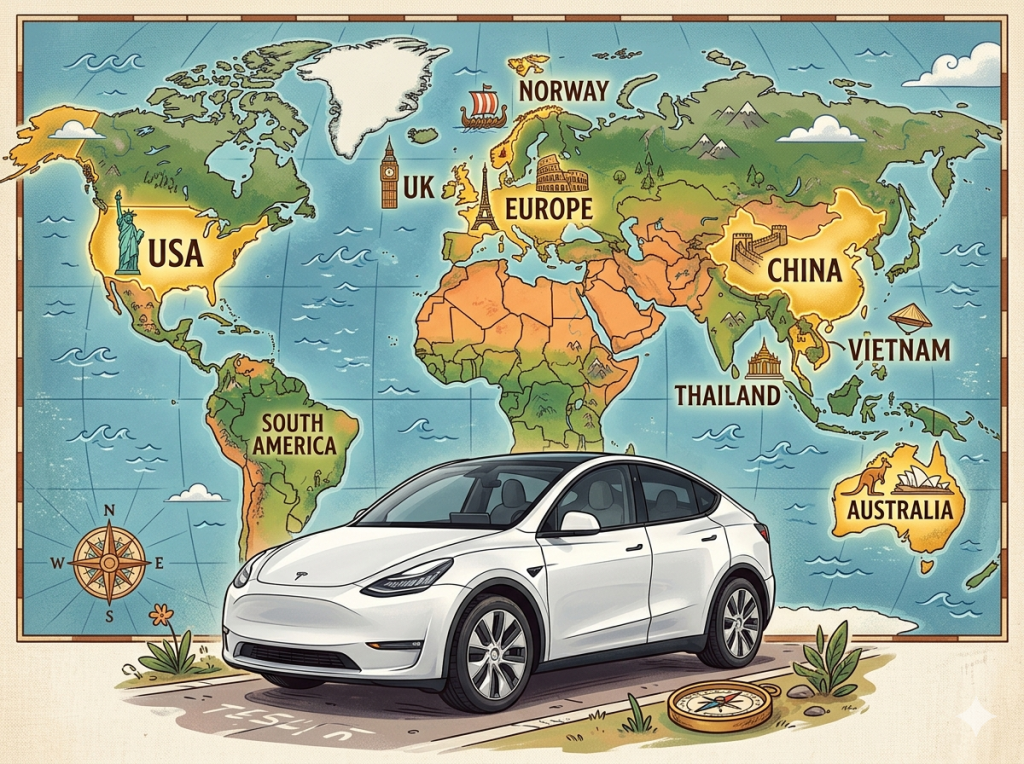

- Norway 97% — Almost all new cars sold are electric. The world’s most advanced EV market — a glimpse of what’s coming.

- China 55% — NEV share in 2025. April 2026 data shows a record 60%+ monthly share. The world’s manufacturing engine.

- Europe 28% — BEV share rose sharply in 2025, up 30%+ on the prior year, driven by tighter CO₂ standards.

- UK 23.4% — 473,348 new BEVs registered in 2025, the first year total new cars exceeded 2 million since pre-pandemic.

- USA 10% — Holding around 10% share as federal tax credits end and Chinese models remain locked out behind tariffs.

- Vietnam 40% — VinFast’s affordable EVs drove penetration from near zero in 2020 to over 40% by mid-2025.

- Thailand 28% — EV sales up 70% in 2025. The EV3.5 scheme and Chinese imports are transforming Southeast Asia’s second-biggest market.

- Australia 20% — BEV market share hit a record 20% in May 2026. Up from just 7.4% BEV share for full-year 2024

The leaders: Norway, China, and Europe’s regulatory push

Norway remains the benchmark that every other country is chasing. With around 97% of all new car sales being electric in 2025, the Nordic nation is essentially post-petrol already. Its success was built on decades of consistent policy: tax exemptions, toll-free roads, free parking, and charging infrastructure that arrived before, not after, mass adoption. Norway proves that EV transitions don’t happen organically — they are engineered.

China’s story is different but equally dramatic. Chinese automakers now supply around 60% of all electric cars sold worldwide, and domestically, EVs (including plug-in hybrids) accounted for nearly 55% of all car sales in 2025. The country’s April 2026 monthly data showed a record high of over 60% EV share. BYD alone sold 4.6 million new energy vehicles globally in 2025. The sheer scale of China’s industrial output — over three-quarters of the world’s almost 22 million electric cars were produced there — means it will continue to shape pricing and availability in every market it reaches, including ours.

Europe is accelerating hard, driven less by consumer enthusiasm than by regulatory compulsion. Tightened EU CO₂ standards pushed European EV sales up more than 30% in 2025 to reach 28% of total sales. In Germany, the UK, and France, manufacturer discounting has been fierce — UK carmakers reportedly discounted BEVs by over £5 billion across 2025 to meet ZEV mandate targets. And in early 2026, with petrol prices spiking sharply on Middle East tensions, European consumers began bringing purchases forward, adding fuel to an already burning market.

The laggard: why the USA is falling behind

The United States presents the sharpest contrast to global trends. Despite being the world’s second-largest car market, EV share has hovered stubbornly around 10% — and it is now under pressure from policy reversal rather than consumer reluctance alone. The ending of EV tax credits, the effective removal of CAFE standard penalties, and a continued 100% tariff on Chinese-built vehicles have combined to create a uniquely hostile environment for EV uptake. US quarterly EV sales set a record in Q3 2025, only to fall away sharply in Q4 as incentives shifted.

Canada tells a similar story from a slightly different angle: EV share actually fell from nearly 17% in 2024 to around 11% in 2025, driven by the ending of a federal rebate programme. North America is the only major region where policy is actively working against the trend rather than with it.

Australia: from laggard to accelerating

For much of the past decade, Australia sat near the bottom of EV adoption rankings among wealthy nations. The criticisms were familiar and largely fair: no fuel efficiency standards, no meaningful federal purchase subsidies, a thin model range, and a charging network that made anything beyond city driving a genuine act of faith.

That story is changing, and changing fast.

Australia sold a record 156,753 electric vehicles in 2025 — a 38% jump on the prior year — with EVs making up 13.1% of all new car sales. Battery electric vehicles (BEVs) accounted for 103,269 of those, an 8.3% share of the total market, while plug-in hybrid (PHEV) sales more than doubled to 53,484 units. Then, in May 2026, battery electric vehicles hit a landmark 20% monthly market share for the first time. When you include PHEVs and conventional hybrids, nearly half of all new vehicles delivered in May 2026 came with some form of electrification. Petrol and diesel sales, by contrast, fell year-on-year by more than 30% and 26% respectively in that same month.

What’s driving the surge? Several forces are converging. The federal government’s New Vehicle Efficiency Standard (NVES), which commenced on 1 January 2025, has pushed manufacturers to supply more efficient models or face penalties — and it’s working. The range of available EVs has expanded dramatically, with Chinese brands like BYD, Geely, Zeekr, Chery (Omoda Jaecoo), and GWM establishing significant presence. BYD ranked third overall in Australian new car sales year-to-date through May 2026, recording a 120% increase. And rising fuel prices, sharpened by Middle East tensions, have handed the cost-of-ownership argument directly to EVs — at current prices, the average Australian driver saves roughly $2,000 a year in fuel alone by switching.

But how does Australia compare globally?

Honestly? We are no longer embarrassingly behind, but we are still mid-table. Australia’s full-year 2025 BEV-only share of 8.3% is similar to South Korea and well ahead of where the US was in 2022. But it is roughly where Europe was in 2021, and well behind where China was even in 2019. We are running a similar race, four or five years behind the leaders.

The structural disadvantages that held us back — no local manufacturing, right-hand drive limiting model availability, vast distances making range anxiety acute, and a strong cultural attachment to utes and SUVs — have not disappeared. The Toyota HiLux and Ford Ranger still sit atop the sales charts. Compelling electric alternatives for the workhorse ute segment remain thin, and the charging network, while growing, still has meaningful gaps in regional areas. Infrastructure Victoria flagged charging rollout as the “next critical pressure point” for sustained uptake, a warning echoed by FCAI chief Tony Weber in mid-2026.

The trajectory, however, has unmistakably changed. Analysis of BEV sales growth since 2010 suggests Australia could approach 80% EV market penetration by 2030 if the current exponential curve holds — a scenario that would have been dismissed as fantasy just three years ago.

State by state: the patchwork of Australian EV policy

One of the peculiarities of Australia’s EV transition is how much it is being shaped — and occasionally hampered — at the state level. There is no national ban on petrol or diesel car sales, but the policy landscape varies dramatically by jurisdiction.

- ACT — Hardest-line position nationally. Targets 80–90% ZEV new car sales by 2030, full ban on new petrol/diesel sales by 2035. Taxi and rideshare fleets to be zero-emission by 2030. Government fleet fully electric where fit for purpose.

- Victoria — Target of 50% zero-emission new car sales by 2030 and 100% by 2035. Infrastructure Victoria has recommended stopping new combustion vehicle registrations by 2035. A parliamentary inquiry in 2026 flagged charging infrastructure acceleration as urgent.

- New South Wales — Targets 50% BEV new car sales by 2030, with EVs to be the “vast majority” by 2035. In April 2026, NSW unveiled a $100 million EV strategy focused on regional fast-charging expansion and fleet electrification. The state rebate scheme ended in 2024, but charging investment continues.

- South Australia — Set targets for 50% EV new car sales by 2030 and 100% by 2035. State purchase subsidies and registration exemptions have now ended (June 2025), signalling a shift from incentive-led to mandate-led approach.

- Queensland — The LNP government elected in October 2024 has rolled back the previous Labor government’s EV mandates. The $6,000 ZEV rebate closed September 2024. In 2025, Queensland axed its 2026 EV-only government fleet mandate, replacing it with a broader “emissions reduction” strategy that includes hybrids and E10 fuels.

- Western Australia — Previously targeted 25% EV new car sales by 2026. The $3,500 EV rebate scheme ended May 2025. Focus has shifted to charging infrastructure rather than purchase incentives.

- Northern Territory — One of the few jurisdictions with active live incentives in 2026: free BEV and PHEV registration extended to June 2027, plus up to $1,500 stamp duty concession for EVs under $50,000.

The divergence between the ACT — which is effectively implementing a mini-Norway policy — and Queensland, which has moved sharply in the opposite direction, illustrates the incoherence that the EV Council and industry groups have repeatedly flagged as a drag on national progress. The NVES at the federal level is the most significant supply-side reform in Australia’s history, but it does not mandate a sales ban — it incentivises manufacturers to bring more efficient vehicles to market or face penalties. Demand-side policy, from states and territories, remains patchy.

The Committee for Sydney’s 2027 diesel ban proposal, while not yet legislated, signals where urban policy thinking is heading. Low-Emission Zones are increasingly common in European cities — Paris, Madrid, Athens — and Australian cities are watching. It is not hard to imagine inner-city councils in Melbourne and Sydney following suit within the decade.

What comes next

The IEA projects global EV sales will reach 23 million in 2026, representing around 28% of all new car sales. Europe is forecast to lead major market growth, with one in three cars sold expected to be electric. China is set to push toward 60% EV share. In Australia, if Q1 2026’s near-doubling of sales versus Q1 2025 holds for the full year, we could finish 2026 around 15–16% BEV share — with total electrified vehicles (including PHEVs and hybrids) potentially nearing half of all new cars sold.

The petrol car is not dead. Not yet. The Toyota HiLux will sell in significant volumes for years to come, regional Australia needs practical electric alternatives that do not yet exist at scale, and the second-hand market means ICE vehicles will remain on our roads well into the 2040s. But the trajectory of new car sales is clear, and the pace of that trajectory is accelerating.

For everyday Australians, the shift is becoming harder to ignore — at the petrol bowser, in the car park, and increasingly on the price tag of a new car. Whether you are an enthusiast or a sceptic, one thing is certain: the next time you buy a car, the conversation will be very different to the last time you did.

Even without any new policy announcements, the global fleet of EVs is projected to grow more than sixfold by 2035 from 2025 levels — to as many as 510 million vehicles worldwide.

IEA Global EV Outlook 2026

Leave a comment